The Real Impact of AI in P&C Claims – Risk & Insurance

The best of R&I and around the web, handpicked by our editors.

White papers, service directory and conferences for the R&I community.

Web replica of the print magazine.

Jim Sorrells brings over 35 years of experience in the P&C insurance industry, including 26 years leading claim organizations at a major carrier. As Sales Director for P&C Insurance at DigitalOwl, he is revolutionizing medical records analysis for Bodily Injury, Uninsured Motorist, and Workers’ Compensation claims.

The property & casualty claims industry is reaching a pivotal moment in the adoption of artificial intelligence (AI). What was once viewed as a future-state transformation is now actively reshaping some of the most complex and consequential areas of claims operations, particularly bodily injury evaluation, workers compensation claim management, and claims litigation.

Injury claims have always demanded significant human expertise because they are fundamentally information problems. A single file may contain thousands of pages of medical records, competing provider narratives, prior injuries, evolving treatment plans, attorney demands, and inconsistent documentation spread across multiple systems and formats. Historically, claims professionals have had to manually synthesize this information under tight timelines while simultaneously managing reserves, litigation exposure, negotiation strategy, and customer outcomes.

AI solutions are now rapidly organizing and analyzing large volumes of medical information, producing clear insights, surfacing inconsistencies, identifying potential severity indicators, and accelerating demand evaluation. What once required hours or days of manual review can be completed in minutes with greater accuracy and quality for every claim professional in an organization. AI enables claim professionals and litigation teams to focus more directly on judgment, negotiation, exposure analysis, and resolution strategy. In many organizations, this is beginning to fundamentally alter how claims are evaluated.

Property & casualty claim organizations face indemnity and expense leakage that often stems from inconsistent evaluations, excessive treatment durations, duplicate billing, incomplete investigations, or missed details buried deep within claim documentation. AI can surface these issues earlier in the claim lifecycle, improving both investigative precision and overall claims consistency, enabling claim organizations to attack and improve ordinary leakage. This is an impactful area where AI Value Realization can be measured.

AI is changing claim management processes, and the strategic value is not simply speed, but clarity in the evaluation and quality of the decision. For claims executives and litigation leaders, this marks a pivotal moment. Rising medical complexity, expanding litigation activity, staffing pressures, and increasing claim severity are forcing organizations to reevaluate how claims professionals spend their time and where expertise delivers the greatest value.

AI is emerging not as a replacement for human judgment, but as a force multiplier. AI-based capabilities are now analyzing structured and unstructured information in injury claims, delivering efficiency and accuracy for claim professionals assigned to evaluate them. What makes this so important is not simply the volume of claims activity. It is the sheer complexity of the decisions involved.

The greatest operational gains are emerging in environments defined by high-severity exposure, large volumes of unstructured information, and increasing decision complexity. Injury claims sit squarely at the center of that challenge. As a result, bodily injury evaluation has become the leading edge of AI transformation across the claims industry. The new AI capabilities will improve early case assessment, reserve confidence, reliable claim insights, defense strategy, and fully informed decision-making.

Claims professionals do not want technology that replaces expertise. They want technology that allows expertise to operate more effectively in increasingly complex environments. The carriers that recognize this dynamic, and lead accordingly, will define the next generation of injury claims performance.

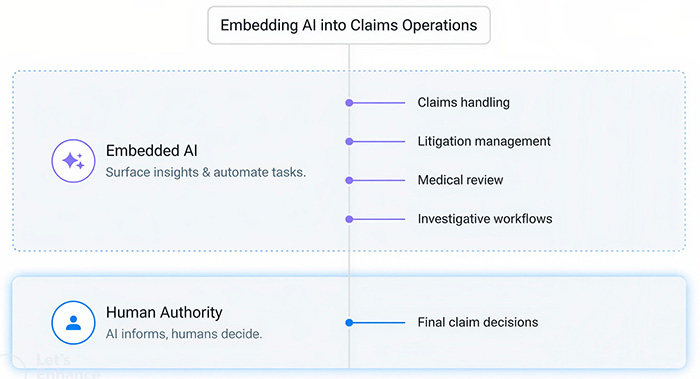

The organizations seeing the strongest results are not approaching AI as a standalone technology initiative. They are embedding it into the operational fabric of claims handling, litigation management, medical review, and investigative workflows while preserving human authority over final claim decisions. That distinction matters.

From medical record review and injury evaluation to reserve setting, litigation management, and claim resolution, the real impact of AI in P&C claims is better decision-making. Organizations that use AI to surface critical insights earlier can reduce uncertainty, improve consistency, and make more informed decisions at every stage of the claim. AI is becoming the infrastructure that enables those decisions at scale. &

Risk Insiders are an unrivaled group of leading executives focused on the topic of Risk. They share their insights and opinions – and from time to time their pet peeves and gripes.

Each Risk Insider is invited to publish based on their expertise, passion and/or the quality of their writing. The only rules are no selling and no competitor put-downs.

The views expressed in this article belong to the author and are not an editorial opinion of Risk & Insurance.

Irina Simpson discusses preparing the industry for mental health claims, an aging workforce, and the talent crisis through AI-enabled platforms and aggressive recruitment of digital natives.

The latest people news in the industry today.

Cumulative losses from severe convective storms now exceed those from hurricanes, challenging the traditional classification of these events as ‘secondary perils,’ according to Allianz Commercial.

From AI integration to nuclear verdicts and home-based care, health care executives face unprecedented disruption, the Doctors Company reports.

Product liability risks are entering a new phase of complexity. Pricing pressures remain front and center, even as segments of the market begin to moderate. Capacity continues to fluctuate, attachment points remain elevated and underwriting discipline has tightened across higher hazard general liability and excess and umbrella layers.

Recent data reflects that reality. While U.S. commercial insurance pricing trended downward throughout 2025, insureds with significant product liability exposures continue to face challenges in securing optimal placements. A 2025 industry survey shows that 86% of independent insurance agents report challenges with market access and product availability as insurance carriers adjust capacity and underwriting strategies, highlighting that access to coverage limits remains limited for many complex risks.

Beneath these conditions lies a deeper issue: escalating loss costs. Social inflation continues to drive severity, with U.S. liability claims increasing 57% over the past decade due to rising litigation and large jury verdicts. These trends are reshaping how carriers deploy capacity and how clients access coverage.

While the market shows signs of softening, the underlying cost dynamics remain unchanged. “In an environment shaped by inflation, supply chain disruption and litigation volatility, these pressures are not only influencing pricing but also reshaping how organizations think about risk ownership and financing structures,” said Seth Hollis, head of specialty general liability at The Hanover. “Borrowed capacity is only one part of the equation. Retained risk is increasingly becoming another.”

For larger, well-managed organizations, self-insured retentions (SIRs) can serve as a powerful strategic lever, improving cost control and supporting long-term program stability. This not only serves as a strong selling point for agents but also enables them to better position clients within a challenging market.

Seth Hollis, Head of Specialty General Liability, The Hanover

Product liability presents a risk profile that often aligns well with retained risk strategies.

Many organizations experience a pattern of predictable, lower-severity claims, while more catastrophic losses remain infrequent but impactful. Traditional insurance structures tend to price toward those high-severity events, driving premium costs even when day-to-day loss activity remains manageable.

For organizations with the right financial and operational profile, this presents a risk management opportunity. “Retaining a more predictable layer of risk can improve efficiency and total cost of risk over time, particularly for companies with strong safety controls and claims oversight,” Hollis said. “These organizations typically combine financial strength with operational discipline, supported by consistent cash flow, credible claims data and a long-term view of risk financing.”

In practice, SIR strategies can take multiple forms depending on the organization’s goals and risk profile. For example, a manufacturer with more frequent, predictable claims may retain a defined layer of risk, while another manufacturer facing less frequent but more severe claims may use an SIR to manage volatility while preserving protection for catastrophic losses. Larger commercial accounts may also use SIRs to gain greater influence over claims management outcomes, using retention to more closely align financial and operational controls.

The key is intentionality. SIRs should be designed around a well-understood risk profile, not introduced as a default response to market pressure.

From a carrier perspective, SIR structures also introduce alignment. When insureds manage claims within their retention, they tend to focus on preventing losses, handling defense strategically, and resolving matters more quickly. This alignment can lead to more sustainable results across the account.

SIRs are often associated with premium savings — and for good reason.

By assuming a portion of risk, insureds can reduce the amount of exposure transferred to the carrier, which typically results in lower upfront premium.

However, that shift also introduces greater financial responsibility. Losses within an SIR are funded directly by the insured and may not be subject to an aggregate cap, requiring organizations to maintain adequate reserves and be prepared to absorb multiple losses within a policy period.

For organizations equipped to manage that responsibility, the value of an SIR extends beyond immediate cost savings:

Amid ongoing economic uncertainty and litigation volatility, these benefits can help organizations achieve more consistent and predictable risk outcomes.

The effectiveness of an SIR program ultimately depends on claims execution.

Managing losses within a retention requires discipline, speed and coordination. “Organizations need the ability to respond quickly to incidents, engage legal resources effectively and resolve claims before costs escalate.” Hollis said. This requires dedicated internal risk management leadership or strong alignment with third-party administrators, supported by clearly defined escalation protocols for more complex claims. A consistent legal strategy, backed by experienced counsel, plays a critical role in maintaining control over outcomes, while ongoing monitoring of claim trends helps ensure that lessons learned are continuously applied.

Even above the retention, carrier expertise remains essential. It provides loss analytics, benchmarking insights and strategic guidance that support the retained layer, help protect excess policies and drive a lower total cost of risk over time.

When these elements are aligned, SIR programs can perform as intended — improving outcomes at both the primary and excess layers.

For independent insurance agents and brokers, SIRs represent an opportunity to elevate the conversation around risk management for the right clients.

The most effective discussions move from “taking on more risk” to focusing on structuring risk more strategically. This includes aligning retention levels with a client’s operational realities and financial tolerance, identifying losses that may already be absorbed indirectly through inefficiencies or premium structure, and assessing readiness to manage claims within a retention framework. SIRs can be thoughtfully positioned as a proactive strategy rather than a reactive adjustment.

There are also clear advantages for agents. SIR solutions are not widely utilized across the middle market, creating differentiation in how programs are structured. As clients grow in size and sophistication, SIRs offer a pathway to evolve coverage without displacing existing relationships.

“This evolution supports long-term partnerships, allowing agents to guide clients from more traditional risk transfer agreements into increasingly sophisticated risk financing strategies over time.” Hollis said.

Carrier selection becomes especially important in SIR programs.

Not all insurance carriers are equipped to support retained risk structures, particularly in complex product liability environments. Even among those that can, many limit loss-sensitive program offerings to national account clients, where qualifications often depend on workers’ compensation being structured on a loss-sensitive basis. “The most effective partners bring a combination of specialized underwriting expertise in product liability and dedicated claims resources that extend beyond traditional coverage,” Hollis said. “They also provide loss control and risk solutions that help insureds better manage exposures within the retention.”

Some carriers, like The Hanover, have dedicated complex general liability teams that can offer SIR structures on general liability programs for a range of customers. They can also maintain guaranteed cost structures for other lines, allowing clients to take on risk selectively where it aligns with their strategy. These capabilities enable more tailored program design as client needs evolve.

In complex liability segments, specialization matters. Precision in underwriting, claims and risk advisory support can significantly influence outcomes across the entire insurance program.

Self-insured retentions are not a universal solution, but in today’s product liability landscape, they are increasingly relevant. Market dynamics will continue to evolve, while underlying loss trends — driven by litigation costs and severity — remain persistent. Organizations that take a deliberate approach to retained risk today are better positioned to navigate the market cycles of tomorrow.

For qualified insureds, SIRs can improve access to coverage, stabilize costs and introduce greater control over claims outcomes. For agents and brokers, this presents an opportunity to grow alongside clients by delivering more value-added strategic advice and placing business more effectively in challenging markets. Partnering with carriers like The Hanover that have the expertise and flexibility to support retained risk structures is critical. Together, these relationships help build insurance programs that are more resilient and better meet customer needs.

To learn more, please visit: https://www.hanover.com/![]()

![]()

This article was produced by the R&I Brand Studio, a unit of the advertising department of Risk & Insurance, in collaboration with The Hanover Insurance Group. The editorial staff of Risk & Insurance had no role in its preparation.

![]()

![]()

source

This is a newsfeed from leading technology publications. No additional editorial review has been performed before posting.

Turn insight into action with CDO TIMES.

CDO TIMES helps executives move from AI awareness to AI execution through practical frameworks, tools, executive research, and advisory support.

Explore the Frameworks

Continue with Enterprise AI 2030, HI + AI = ECI, AI Governance, and executive playbooks.

Explore Enterprise AI 2030 →Use the Free Tools

Assess readiness, estimate AI ROI, model AI costs, and prioritize AI initiatives.

Open Executive Tools →Read the Book

Explore the HI + AI = ECI leadership model in The AI-Ready Leader.

Order The AI-Ready Leader →Go deeper with CDO TIMES Pro.

Unlock premium research, executive playbooks, templates, advanced tools, and member-only briefings.

Need executive help?

Explore advisory, workshops, fractional CIO/CDO/CISO/CAIO support, and AI operating model design.

Explore Advisory →Attend executive events

Join leadership forums, executive dinners, webinars, and strategic AI briefings.

View Events →Build AI capability

Use CDO TIMES Academy for executive learning, AI leadership development, and implementation training.

Explore Academy →