SK Hynix Has a Major Warning for Micron Technology Stock Investors – The Motley Fool

The supply shortage has led to a sharp spike in memory prices, and Micron Technology (MU +8.80%) has been one of the biggest beneficiaries of the favorable demand-supply dynamic in this industry. Micron stock has jumped by 1,570% over the past three years, fueled by phenomenal growth in revenue and earnings.

The good news for Micron investors is that the memory shortage is expected to persist through 2030, according to the chairman of memory giant SK Hynix's parent company. This could set the stage for further growth in Micron's revenue and earnings. However, SK Hynix's latest announcement of rapidly increasing production capacity may undermine Micron's momentum.

Image source: Micron Technology.

South Korean semiconductor giant SK Hynix is among the world's leading memory manufacturers, alongside Samsung and Micron. According to Counterpoint Research, SK Hynix controlled 29% of the global dynamic random-access memory (DRAM) market in the first quarter of 2026. Its share of the NAND flash storage market stood at 18%.

It is worth noting that SK Hynix is the largest vendor of high-bandwidth memory (HBM) with a share of 58% in the previous quarter. HBM demand has taken off over the past three years as it is being deployed extensively in AI accelerator chips. Moreover, the booming HBM demand has created a supply shortage in the memory industry as it requires 3x the wafer capacity required to produce conventional chips.

However, SK Hynix has been losing ground in the memory market to competitors. Its HBM share slipped by 11 percentage points year over year in Q1, while its share of conventional DRAM was down by seven points. It also lost two percentage points in the NAND flash storage market. Not surprisingly, the company is now aiming to double its wafer capacity over the next five years to capture the strong memory demand.

Speaking at the Computex conference held earlier this month, SK Group chairman Chey Tae-won (via Reuters) remarked that the company will "double the whole capacity over the next five years." This seems like a warning for Micron Technology, which has benefited significantly from the memory supply shortage, resulting in massive margin expansion.

But will SK Hynix's move to add more capacity derail Micron's momentum?

Ideally, the addition of new production capacity should help arrest the rapid jump in memory prices. After all, SK Hynix is one of the biggest players in this space, and its aim of doubling capacity means investors can expect a significant expansion in supply. However, demand for memory chips is also poised to increase rapidly over the next five years.

SK Hynix itself expects that the supply bottlenecks in the memory industry won't go away until 2030. Additionally, it expects HBM demand to grow by 30% annually through the end of the decade. We have already seen that HBM requires significantly more wafer capacity than conventional memory chips, which means the new capacity SK Hynix brings online will be quickly absorbed.

Additionally, sales of smartphones and personal computers (PCs) are declining due to the memory bottleneck. Market research firm IDC expects smartphone sales to drop by almost 14% this year, followed by a 1.1% drop next year. The PC market is expected to shrink by 11% this year. Declining sales, caused by a spike in memory prices, will eventually create pent-up demand for memory chips in PCs and smartphones.

Investors, therefore, shouldn't fret about the new memory capacity that's coming online. In fact, Micron itself is on track to spend over $25 billion on capital expenditure this fiscal year compared to $13.8 billion in the previous one. Management noted on the company's March earnings call that the DRAM requirement in AI chips has doubled, and it is seeing a jump in memory demand in edge AI devices and AI-capable smartphones and PCs as well.

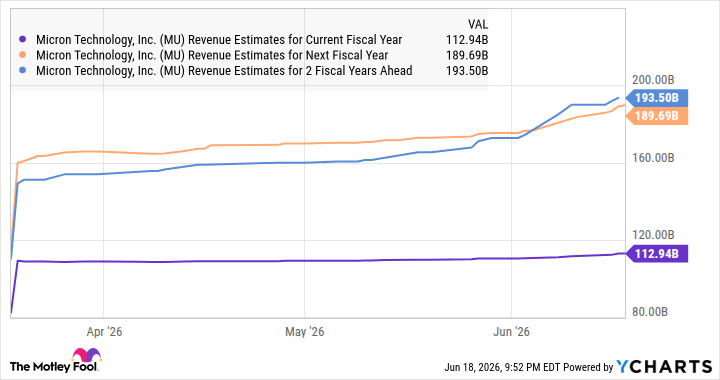

So, the favorable demand-supply environment prevailing in the memory industry seems sustainable over the long run. This explains why analysts have been raising their revenue growth expectations for Micron for the next couple of years.

Data by YCharts

Don't be surprised if these estimates move higher due to robust memory demand over the long run. Also, this AI stock is trading at an incredibly attractive price/earnings-to-growth (PEG) ratio of 0.33, according to Yahoo! Finance. This ratio is calculated by dividing a company's trailing earnings multiple by the projected annual earnings growth it could clock over the next five years.

A reading below 1 means that the stock is undervalued, and Micron's PEG ratio is well below that mark. So, investors can still buy this growth stock, as rapidly growing memory demand should ensure it continues to grow at a healthy rate over the long run.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Micron Technology. The Motley Fool has a disclosure policy.

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.

Making the world smarter, happier, and richer.

© 1995 – 2026 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.

About The Motley Fool

Our Services

Around the Globe

Free Tools

Affiliates & Friends

The Korean memory giant is planning to significantly increase its production capacity over the next five years.

source

This article was autogenerated from a news feed from CDO TIMES selected high quality news and research sources. There was no editorial review conducted beyond that by CDO TIMES staff. Need help with any of the topics in our articles? Schedule your free CDO TIMES Tech Navigator call today to stay ahead of the curve and gain insider advantages to propel your business!

Turn insight into action with CDO TIMES.

CDO TIMES helps executives move from AI awareness to AI execution through practical frameworks, tools, executive research, and advisory support.

Explore the Frameworks

Continue with Enterprise AI 2030, HI + AI = ECI, AI Governance, and executive playbooks.

Explore Enterprise AI 2030 →Use the Free Tools

Assess readiness, estimate AI ROI, model AI costs, and prioritize AI initiatives.

Open Executive Tools →Read the Book

Explore the HI + AI = ECI leadership model in The AI-Ready Leader.

Order The AI-Ready Leader →Go deeper with CDO TIMES Pro.

Unlock premium research, executive playbooks, templates, advanced tools, and member-only briefings.

Need executive help?

Explore advisory, workshops, fractional CIO/CDO/CISO/CAIO support, and AI operating model design.

Explore Advisory →Attend executive events

Join leadership forums, executive dinners, webinars, and strategic AI briefings.

View Events →Build AI capability

Use CDO TIMES Academy for executive learning, AI leadership development, and implementation training.

Explore Academy →